Fixed Rates Made for Instant Refinancing

Fixed Rates Made for Instant Refinancing

At Liquid, we're creating a new lending model that cross-collateralizes loans with both traditional real estate and Bitcoin. Our goal is to reduce risk for lenders and borrowers by pairing real estate's comparatively stable valuations with Bitcoin's high liquidity and growth potential.

Real Estate vs. Bitcoin: Stability vs. Volatility

Real Estate Stability

Traditional real estate is typically perceived as relatively stable compared to Bitcoin because it's not traded on a 24/7 open market, and its valuation changes are usually formalized through periodic appraisals—often just once a year.

Bitcoin Volatility

Bitcoin, on the other hand, is a highly liquid asset with over $30 billion in daily trading volume. Its price can fluctuate significantly in short periods, driven by news, market sentiment, or macroeconomic factors.

The Core Thesis: Early Stages of Bitcoin Adoption

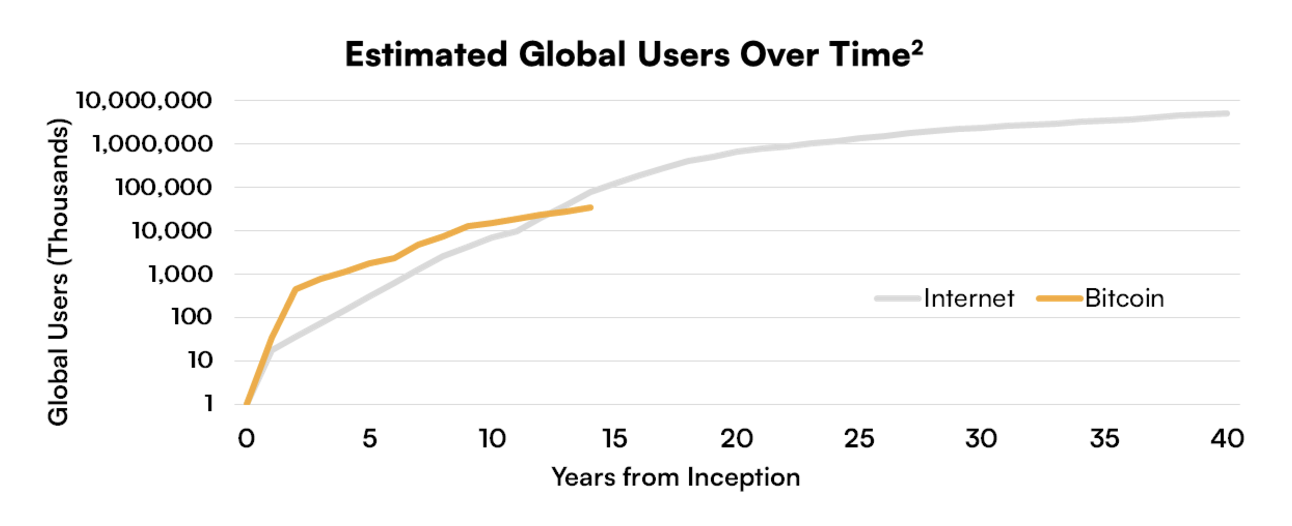

We believe Bitcoin is still in its early stages of adoption, supported by growing interest from institutional players and nation-states. As shown in adoption-curve comparisons, Bitcoin's growth trajectory resembles that of the internet: both began as abstract yet transformative technologies.

Over time, we anticipate broader retail, institutional, and even nation-state adoption. We are already beginning to see this with:

- 40% of American adults owning cryptocurrencies

- BlackRock launching a Bitcoin ETF that reached $50B in assets 5x faster than the previous record holder

- Nations like El Salvador establishing a strategic Bitcoin reserve

As Bitcoin's value grows, the loan's collateralization ratio improves, reducing risk and enabling us to offer lower interest rates to borrowers.

Cross-Collateralized: A Unique Safeguard

An additional feature of Liquid's model is that our loans are cross-collateralized with Bitcoin. Even if Bitcoin were to experience a severe drop—or, hypothetically, go to zero—traditional real estate collateral would still maintain loan-to-value ratios typically required by conventional lenders. As a borrower, you are not personally "on the hook" for the investment loss in Bitcoin because the total collateral from both assets covers the loan's risk requirements. However, this is highly unlikely. Historically, the lowest annual returns Bitcoin has produced over a 4 year period is 20%+. The average annual returns over the last 10 years has been 80%+.

Navigating Bitcoin's Short-Term Volatility

Although we see a long-term upward trajectory for Bitcoin, its price can vary significantly in the short term. These fluctuations affect collateralization ratios and, by extension, any associated variable interest rates. To protect borrowers from abrupt changes and uncertainty in their debt expenses, Liquid will initially offer only fixed-rate loans designed for frequent refinancing. This way, as risk profiles improve, borrowers can secure better terms without prohibitive fees.

Fixed vs. Floating Rates: Key Differences

Before getting into the rationale for starting with fixed rate loans, it's important to understand why borrowers would choose a fixed or floating rate loan.

Floating-Rate Loans

Definition:

Floating-rate loans have interest rates that adjust based on a benchmark rate, commonly influenced by the U.S. Federal Reserve's Federal Open Market Committee (FOMC). If the Fed lowers its target range by 0.25%, floating loan rates generally decrease by a similar margin—and vice versa when the Fed raises rates.

Why Choose Floating?

- Lower Rates: Floating-rate loans typically start at lower interest rates.

- Short-Term Savings: For shorter-term projects, the potential savings from lower initial rates may outweigh the risk of later increases.

- Falling Rate Environment: The borrower anticipates Fed rate cuts.

- Flexible Structures: Fewer or more flexible prepayment penalties, making it easier to refinance or sell in the near term.

Fixed-Rate Loans

Definition:

Fixed-rate loans lock in an interest rate for the entire term, offering no surprises in monthly or quarterly payments.

Why Choose Fixed?

- Predictable Expenses: No interest rate risk makes budgeting straightforward.

- Shield Against Rate Hikes: You're protected if the Fed raises rates.

- Easier Long-Term Planning: Stable debt service simplifies underwriting and can make financial projections more accurate.

Common Drawbacks of Traditional Fixed-Rate Loans—And Liquid's Solutions

Even though Liquid supports fixed rates initially, we recognize traditional fixed-rate loans often carry certain disadvantages. Here's how we address them:

1. Prepayment Penalties

The Problem:

Many fixed-rate loans have steep prepayment penalties (e.g., yield maintenance, defeasance fees) to compensate lenders for lost future interest when a borrower refinances or repays early. These fees can deter refinancing, selling, or restructuring.

Liquid's Solution:

Our system is built for frequent and consistent refinancing. Borrowers upload asset performance data on a monthly cadence, and we monitor collateralization ratios in real time. If your asset risk declines (e.g., improved collateral ratio), we believe you deserve a lower rate. Leveraging our AI-driven diligence, we are able to cut the cost of refinancing to just 0.05–0.1% of the loan value, which is significantly below the typical 1–3% charged by traditional banks. Additionally, refinancing can be done with a click of a button, saving borrowers months of manual due diligence.

2. Higher Initial Interest Rates

The Problem:

Banks issue fixed-rate loans at higher rates to offset the interest rate risk. If market rates rise, the bank is locked into a lower rate, so they charge more at the outset.

Liquid's Solution:

We don't believe in profiting from purely macro-rate speculation. Instead, our focus is on meritocratic measures of success such as asset performance and collateralization ratios. This means that if your risk profile improves, we'll lower your rate accordingly rather than keeping it artificially high. By prioritizing the fundamental health and performance of the collateral, we ensure that our interest rates accurately reflect the true risk of the loan, providing fair and competitive rates without unnecessary premiums.

3. Missing Out on Lower Rates

The Problem:

When market interest rates drop, fixed-rate borrowers miss out unless they pay hefty refinancing penalties. This can make them less competitive compared to floating-rate loans.

Liquid's Solution:

Our thesis is that Bitcoin's price will appreciate in the long run. As it does, the improved collateral ratio naturally lowers interest rates. Furthermore, if general market rates also fall, capital is likely to flow into riskier assets like Bitcoin, potentially raising collateral value further and pushing rates down even more. Because refinancing with Liquid is inexpensive and streamlined, you're never locked into a higher rate and can take advantage of lower rates without the burden of significant penalties.

Looking Ahead: Floating Rates

While our initial focus is on offering a fixed-rate standard for stability, we plan to introduce floating-rate loan products in the future. Floating rates come with added complexities—like adjusting monthly payments and more intricate risk monitoring—which our AI-driven platform can handle. However, we want to ensure the best possible user experience from day one, and fixed rates are the simplest way to provide that initial certainty.

Conclusion

At Liquid, we envision a future where real estate and Bitcoin work in harmony to create efficient, transparent, and borrower-friendly lending solutions. By combining real estate's relative stability with Bitcoin's high liquidity and growth potential—and overcollateralizing our loans—we enable a structure that benefits both borrowers and lenders. Our AI-driven underwriting keeps refinancing costs minimal, ensuring you can adjust your financing strategy with ease as market conditions change.

Disclaimer: The content in this blog post is for informational purposes only and should not be considered financial or investment advice. Always do your own research and consult with qualified professionals before making any financial decisions.